Monday, March 7, 2011

Sunday, February 6, 2011

जुबान पर नहीं, करें कागजों पर भरोसा-प्रॉपर्टी-बिज़नस-Navbharat Times

जुबान पर नहीं, करें कागजों पर भरोसा-प्रॉपर्टी-बिज़नस-Navbharat Times

आज के दौर में जब भाई भाई को धोखा देने से बाज नहीं आता है, तो अनजान की क्या कहें! अगर आपको कोई प्रॉपर्टी पसंद आ गई है और आप उसके लिए बयाना भी दे चुके हैं, तो रजिस्ट्री से पहले एग्रीमेंट टू सेल तैयार कराने की सावधानी जरूर बरतें।

अगर आप प्रॉपर्टी बेचने का फैसला कर चुके हैं या फिर खुद कोई प्रॉपर्टी खरीदने जा रहे हैं, तो केवल जुबानी वादे पर ही भरोसा न करें। भले ही दूसरी पार्टी आपकी कितनी ही नजदीकी क्यों न हो! डील फाइनल होते ही सेल डीड तैयार नहीं की जा सकती, लेकिन इससे पहले डील को कानूनी रूप देने के लिए एक अन्य कागजात का सहारा लिया जा सकता है। वह है, एग्रीमेंट टु सेल।

वास्तव में, सेल डीड भी एग्रीमेंट टू सेल की शर्तों के आधार पर ही तैयार की जाती है। यह एग्रीमेंट बॉयर और सेलर के बीच नॉन जूडीशियल स्टाम्प पेपर पर तैयार किया जाता है। यह प्रमाण के रूप में कानूनन मान्य होता है। यह एग्रीमेंट ही कन्वेंस डीड तैयार करने का आधार बनता है।

सेल डीड

'सेल डीड' तैयार करते समय 'एग्रीमेंट टू सेल' का महत्व सामने आता है। एग्रीमेंट में लिखी शर्तों के आधार पर ही सेल डीड तैयार की जाती है। इस प्रकार तैयार सेल डीड बायर और सेलर के बीच साइन की जाती है। इसे रजिस्ट्रार के ऑफिस में रजिस्टर कराना जरूरी होता है। 'सेल डीड' ऐसा लिखित दस्तावेज होता है, जो प्रॉपर्टी के मालिकाना हक के बारे में जानकारी देता है। अगर प्रॉपर्टी के एक से ज्यादा मालिक रहे हैं, तो इसका उल्लेख भी सेल डीड में किया जाता है। साथ ही, डील की कुल कीमत, एडवांस्ड और बैलेंस्ड अमाउंट की जानकारी भी दी जाती है।

सेल डीड के माध्यम से ही पुराना मालिक प्रॉपर्टी पर अपना मालिकाना हक छोड़ने की घोषणा करता है और यह भी बताता है कि प्रॉपर्टी पर किसी किस्म का कोई बकाया नहीं है। दोनों पार्टियों के लिए सेल डीड में लिखी गई शर्तों को मानना कानूनन जरूरी होता है। इससे पहले लिखे गए एग्रीमेंट टू सेल में वे शर्तें लिखी होती हैं, जिनके आधार पर दोनों पार्टियां प्रॉपर्टी की डील करना चाहती हैं। ऐसे में एग्रीमेंट टू सेल तैयार करने से सेल डीड के समय या बाद में कभी भी किसी विवाद से बचा जा सकता है।

क्या लिखें एग्रीमेंट टु सेल में

- दोनों पार्टियों के नाम, स्थायी पते और उम्र

- एग्रीमेंट तैयार करने का दिन, दिनांक और जगह

- दोनों पार्टियों के अधिकार और जिम्मेदारियां

- उन कागजात का संक्षिप्त ब्योरा , जिनके आधार पर सेलर ने प्रॉपर्टी हासिल की थी

- प्रॉपर्टी का सही ब्योरा , जैसे - जगह , साइज , कंस्ट्रक्शन डिटेल आदि

- सेल की कुल रकम का ब्योरा

- पेमेंट का माध्यम और समय

- विभिन्न जिम्मेदारियों , जैसे - अगला पेमेंट , फाइनल डीड आदि के लिए निश्चित समय सीमा

- ट्रांसेक्शन में होने वाले खर्च की जिम्मेदारी किस पार्टी की होगी

- किसी भी पार्टी द्वारा एग्रीमेंट की कोई भी शर्त नहीं मानने पर लगने वाली पेनल्टी

- पजेशन के लिए शर्तें

- सेलर द्वारा यह घोषणा कि उक्त प्रॉपर्टी पर किसी प्रकार का कोई बकाया नहीं है

- गवाहों के नाम , साइन और पते

अगर आप प्रॉपर्टी बेचने का फैसला कर चुके हैं या फिर खुद कोई प्रॉपर्टी खरीदने जा रहे हैं, तो केवल जुबानी वादे पर ही भरोसा न करें। भले ही दूसरी पार्टी आपकी कितनी ही नजदीकी क्यों न हो! डील फाइनल होते ही सेल डीड तैयार नहीं की जा सकती, लेकिन इससे पहले डील को कानूनी रूप देने के लिए एक अन्य कागजात का सहारा लिया जा सकता है। वह है, एग्रीमेंट टु सेल।

वास्तव में, सेल डीड भी एग्रीमेंट टू सेल की शर्तों के आधार पर ही तैयार की जाती है। यह एग्रीमेंट बॉयर और सेलर के बीच नॉन जूडीशियल स्टाम्प पेपर पर तैयार किया जाता है। यह प्रमाण के रूप में कानूनन मान्य होता है। यह एग्रीमेंट ही कन्वेंस डीड तैयार करने का आधार बनता है।

सेल डीड

'सेल डीड' तैयार करते समय 'एग्रीमेंट टू सेल' का महत्व सामने आता है। एग्रीमेंट में लिखी शर्तों के आधार पर ही सेल डीड तैयार की जाती है। इस प्रकार तैयार सेल डीड बायर और सेलर के बीच साइन की जाती है। इसे रजिस्ट्रार के ऑफिस में रजिस्टर कराना जरूरी होता है। 'सेल डीड' ऐसा लिखित दस्तावेज होता है, जो प्रॉपर्टी के मालिकाना हक के बारे में जानकारी देता है। अगर प्रॉपर्टी के एक से ज्यादा मालिक रहे हैं, तो इसका उल्लेख भी सेल डीड में किया जाता है। साथ ही, डील की कुल कीमत, एडवांस्ड और बैलेंस्ड अमाउंट की जानकारी भी दी जाती है।

सेल डीड के माध्यम से ही पुराना मालिक प्रॉपर्टी पर अपना मालिकाना हक छोड़ने की घोषणा करता है और यह भी बताता है कि प्रॉपर्टी पर किसी किस्म का कोई बकाया नहीं है। दोनों पार्टियों के लिए सेल डीड में लिखी गई शर्तों को मानना कानूनन जरूरी होता है। इससे पहले लिखे गए एग्रीमेंट टू सेल में वे शर्तें लिखी होती हैं, जिनके आधार पर दोनों पार्टियां प्रॉपर्टी की डील करना चाहती हैं। ऐसे में एग्रीमेंट टू सेल तैयार करने से सेल डीड के समय या बाद में कभी भी किसी विवाद से बचा जा सकता है।

क्या लिखें एग्रीमेंट टु सेल में

- दोनों पार्टियों के नाम, स्थायी पते और उम्र

- एग्रीमेंट तैयार करने का दिन, दिनांक और जगह

- दोनों पार्टियों के अधिकार और जिम्मेदारियां

- उन कागजात का संक्षिप्त ब्योरा , जिनके आधार पर सेलर ने प्रॉपर्टी हासिल की थी

- प्रॉपर्टी का सही ब्योरा , जैसे - जगह , साइज , कंस्ट्रक्शन डिटेल आदि

- सेल की कुल रकम का ब्योरा

- पेमेंट का माध्यम और समय

- विभिन्न जिम्मेदारियों , जैसे - अगला पेमेंट , फाइनल डीड आदि के लिए निश्चित समय सीमा

- ट्रांसेक्शन में होने वाले खर्च की जिम्मेदारी किस पार्टी की होगी

- किसी भी पार्टी द्वारा एग्रीमेंट की कोई भी शर्त नहीं मानने पर लगने वाली पेनल्टी

- पजेशन के लिए शर्तें

- सेलर द्वारा यह घोषणा कि उक्त प्रॉपर्टी पर किसी प्रकार का कोई बकाया नहीं है

- गवाहों के नाम , साइन और पते

प्रॉपर्टी खरीदते समय कागजात की बात-प्रॉपर्टी-बिज़नस-Navbharat Times

प्रॉपर्टी खरीदते समय कागजात की बात-प्रॉपर्टी-बिज़नस-Navbharat Times

प्रॉपर्टी की खरीदारी से जुड़े कई कागजों का रजिस्ट्रेशन कराना जरूरी होता है। इस बारे में दिशा-निर्देश देने के लिए 'इंडियन रजिस्ट्रेशन एक्ट 1902' बनाया गया है। इसमें स्पष्ट है कि किन कागजात को रजिस्टर्ड कराना जरूरी है और किन्हें नहीं। इस ऐक्ट के अलावा कुछ कागजात का रजिस्ट्रेशन 'दि ट्रांसफर ऑफ प्रॉपर्टी ऐक्ट 1882' के अनुसार भी किया जाता है।

- ' इंडियन रजिस्ट्रेशन एक्ट 1902' के सेक्शन 17 के अनुसार हर मूल्य की प्रॉपर्टी की गिफ्ट डीड रजिस्टर्ड कराना जरूरी है।

- इसी सेक्शन के अनुसार, गैर-वसीयत वाले ऐसे कागजात भी रजिस्टर्ड होने चाहिए, जिनसे अचल संपत्ति में अधिकार, दावा या रुचि साबित हो, इनका हनन हो या इनके संबंध में किसी लेनदेन के बारे में बताया जाए।

- ज्यादातर मॉर्गेज डीड को भी रजिस्टर्ड कराना जरूरी होता है।

- 100 रुपये से कम कीमत में प्रॉपर्टी बेचने पर सेल डीड को रजिस्टर्ड कराने से छूट दी गई है। वास्तव में, यह संभव नहीं होता।

- एक साल से ज्यादा समय की लीज या सालाना किराया तय करने पर इसके कागजात रजिस्टर्ड कराने की बाध्यता है। सालाना किराया तय करने से मतलब जब पूरे साल के लिए किराया तो तय हो जाए, लेकिन लीज का समय निर्धारित न हो।

- ' ईयर टू ईयर' लीज डॉक्यूमेंट के रजिस्ट्रेशन से यह मतलब है कि लीज खुद-ब-खुद एक से अगले साल में प्रवेश कर जाएगी। इस स्थिति में मकान मालिक के पास यह अधिकार नहीं होता कि साल के अंत में बिना नोटिस दिए लीज खत्म कर सके। अगर वह मकान पर फिर अपना कब्जा चाहता है, तो इसके लिए उसे किराएदार को लीज खत्म करने का नोटिस देना होगा। इस तरह के रजिस्ट्रेशन में जरूरी है कि लीज का समय एक साल से ज्यादा हो। यानी अगर कोई लीज एक साल से ज्यादा समय के लिए कराई जाए, तो इसे बाकायदा रजिस्टर्ड कराना जरूरी है।

- ' इंडियन रजिस्ट्रेशन एक्ट 1902' के सेक्शन 49 के अनुसार, रजिस्ट्रेशन के लिए जरूरी कागजात में से अगर किसी को रजिस्टर्ड नहीं कराया जाता है, तो उससे जुड़ी डील कानूनन मान्य नहीं होगी।

- ' दि ट्रांसफर ऑफ प्रॉपर्टी ऐक्ट 1882' के सेक्शन 53 ए के अनुसार दि स्पेसिफिक रिलीफ एक्ट के अंतर्गत बताए गए खास मामलों में गैर पंजीकृत कागजात को भी सुबूत माना जा सकता है

- ' इंडियन रजिस्ट्रेशन एक्ट 1902' के सेक्शन 17 के अनुसार हर मूल्य की प्रॉपर्टी की गिफ्ट डीड रजिस्टर्ड कराना जरूरी है।

- इसी सेक्शन के अनुसार, गैर-वसीयत वाले ऐसे कागजात भी रजिस्टर्ड होने चाहिए, जिनसे अचल संपत्ति में अधिकार, दावा या रुचि साबित हो, इनका हनन हो या इनके संबंध में किसी लेनदेन के बारे में बताया जाए।

- ज्यादातर मॉर्गेज डीड को भी रजिस्टर्ड कराना जरूरी होता है।

- 100 रुपये से कम कीमत में प्रॉपर्टी बेचने पर सेल डीड को रजिस्टर्ड कराने से छूट दी गई है। वास्तव में, यह संभव नहीं होता।

- एक साल से ज्यादा समय की लीज या सालाना किराया तय करने पर इसके कागजात रजिस्टर्ड कराने की बाध्यता है। सालाना किराया तय करने से मतलब जब पूरे साल के लिए किराया तो तय हो जाए, लेकिन लीज का समय निर्धारित न हो।

- ' ईयर टू ईयर' लीज डॉक्यूमेंट के रजिस्ट्रेशन से यह मतलब है कि लीज खुद-ब-खुद एक से अगले साल में प्रवेश कर जाएगी। इस स्थिति में मकान मालिक के पास यह अधिकार नहीं होता कि साल के अंत में बिना नोटिस दिए लीज खत्म कर सके। अगर वह मकान पर फिर अपना कब्जा चाहता है, तो इसके लिए उसे किराएदार को लीज खत्म करने का नोटिस देना होगा। इस तरह के रजिस्ट्रेशन में जरूरी है कि लीज का समय एक साल से ज्यादा हो। यानी अगर कोई लीज एक साल से ज्यादा समय के लिए कराई जाए, तो इसे बाकायदा रजिस्टर्ड कराना जरूरी है।

- ' इंडियन रजिस्ट्रेशन एक्ट 1902' के सेक्शन 49 के अनुसार, रजिस्ट्रेशन के लिए जरूरी कागजात में से अगर किसी को रजिस्टर्ड नहीं कराया जाता है, तो उससे जुड़ी डील कानूनन मान्य नहीं होगी।

- ' दि ट्रांसफर ऑफ प्रॉपर्टी ऐक्ट 1882' के सेक्शन 53 ए के अनुसार दि स्पेसिफिक रिलीफ एक्ट के अंतर्गत बताए गए खास मामलों में गैर पंजीकृत कागजात को भी सुबूत माना जा सकता है

सोसायटी में प्रॉपर्टी का ट्रांसफर-प्रॉपर्टी-बिज़नस-Navbharat Times

सोसायटी में प्रॉपर्टी का ट्रांसफर-प्रॉपर्टी-बिज़नस-Navbharat Times

हाउसिंग सोसायटी के सदस्यों को यह अधिकार होता है कि वे अपना अपार्टमेंट किसी और के नाम ट्रांसफर कर सकें, लेकिन ऐसा करते समय उन्हें सोसायटी द्वारा तय नियम-शर्तों को मानना जरूरी होगा।

यदि कोई सदस्य अपना शेयर और कैपिटल या सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर करना चाहता है, तो उसे ऐसा करने से पहले निर्धारित फॉर्म द्वारा सोसायटी के सेक्रेटरी को इसके बारे में सूचित करना होगा। साथ ही, जिसके नाम पर प्रॉप्रटी ट्रांसफर की जानी है, उसकी स्वीकृति भी लिखित में देनी चाहिए। नोटिस पीरियड सोसायटी के नियम-शर्तों के अनुरूप होता है, जो 15-30 दिनों के बीच कुछ भी हो सकता है। नोटिस मिलने के बाद सेक्रेटरी उसे अगली मीटिंग में कमिटी के सामने पेश करता है, जहां इस पर विचार किया जाता है कि नोटिस देने वाले सदस्य के पास प्राइमा फेसिया (प्रथम दृष्टया) के तौर पर प्रॉपर्टी ट्रांसफर करने का अधिकार है भी या नहीं। कमिटी का जो भी फैसला होगा, उसके बारे में सेक्रेटरी को तीन दिन के भीतर उस सदस्य को सूचित करना होता है।

प्रॉपर्टी ट्रांसफर करने का तरीका

- सोसाइटी मेंबर को अपने शेयर, कैपिटल व सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर करने के लिए शेयर सटिर्फिकेट्स के साथ एक निर्धारित फॉर्म में ऐप्लिकेशन जमा करनी होगी।

- जिसके नाम पर प्रॉपर्टी का ट्रांसफर किया जाना है, सोसायटी में उसकी सदस्यता के लिए एक फॉर्म में ऐप्लिकेशन देनी होगी।

- प्रॉपर्टी ट्रांसफर करने के पीछे क्या ठोस कारण हैं, बताना होगा।

- ट्रांसफर से पहले सोसायटी के प्रति अपनी जिम्मेदारियां पूरी करनी होंगी।

- ट्रांसफर फीस अदा करनी होगी।

- जिस व्यक्ति को मेंबरशिप ट्रांसफर की जानी है, उसकी फीस भी देनी होगी।

- जनरल बॉडी मीटिंग में तय रेट पर प्रीमियम की राशि अदा करनी होगी (यदि ट्रांसफर परिवार के किसी सदस्य, नॉमिनी या फिर उसके लीगल रिप्रजेंटेटिव के नाम किया जा रहा है, तो उस स्थिति में यह शर्त लागू नहीं होती)।

- यदि आवश्यकता हो, तो 'नो ऑब्जेक्शन सर्टिफिकेट' (एनओसी) जमा करना होगा।

मैनेजिंग कमिटी या जनरल बॉडी सदस्यता का आवेदन या शेयर और कैपिटल या सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर का प्रस्ताव एक ही सूरत में इनकार कर सकती है

-यदि कानून के प्रावधानों या सोसायटी के नियमों का पूरी तरह पालन नहीं किया गया हो या फिर इस संबंध में सरकारी निर्देशों की अवहेलना हो रही हो।

- यदि सदस्य को अपनी ऐप्लिकेशन पर तीन महीने तक कमिटी या जनरल बॉडी की तरफ से कोई प्रतिक्रिया नहीं मिलती, तो उस हालत में ऐप्लिकेशन को स्वीकृत मान लिया जाएगा।

- यदि कानून या सोसायटी के नियम-शर्तों की अवहेलना करके कोई ट्रांसफर किया जाता है, तो उसे रद्द करार दिया जाएगा।

हाउसिंग सोसायटी के फ्लैट्स आमतौर पर बेचे नहीं जा सकते, इसके सदस्य अपना शेयर यानी अपार्टमेंट किसी और व्यक्ति के नाम पर ट्रांसफर अवश्य कर सकते हैं। इस प्रक्रिया में किन शर्तों और नियमों को ध्यान रखने की जरूरत होगी, इस पर डालते हैं एक नजर :

हाउसिंग सोसायटी के सदस्यों को यह अधिकार होता है कि वे अपना अपार्टमेंट किसी और के नाम ट्रांसफर कर सकें, लेकिन ऐसा करते समय उन्हें सोसायटी द्वारा तय नियम-शर्तों को मानना जरूरी होगा।

यदि कोई सदस्य अपना शेयर और कैपिटल या सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर करना चाहता है, तो उसे ऐसा करने से पहले निर्धारित फॉर्म द्वारा सोसायटी के सेक्रेटरी को इसके बारे में सूचित करना होगा। साथ ही, जिसके नाम पर प्रॉप्रटी ट्रांसफर की जानी है, उसकी स्वीकृति भी लिखित में देनी चाहिए। नोटिस पीरियड सोसायटी के नियम-शर्तों के अनुरूप होता है, जो 15-30 दिनों के बीच कुछ भी हो सकता है। नोटिस मिलने के बाद सेक्रेटरी उसे अगली मीटिंग में कमिटी के सामने पेश करता है, जहां इस पर विचार किया जाता है कि नोटिस देने वाले सदस्य के पास प्राइमा फेसिया (प्रथम दृष्टया) के तौर पर प्रॉपर्टी ट्रांसफर करने का अधिकार है भी या नहीं। कमिटी का जो भी फैसला होगा, उसके बारे में सेक्रेटरी को तीन दिन के भीतर उस सदस्य को सूचित करना होता है।

प्रॉपर्टी ट्रांसफर करने का तरीका

- सोसाइटी मेंबर को अपने शेयर, कैपिटल व सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर करने के लिए शेयर सटिर्फिकेट्स के साथ एक निर्धारित फॉर्म में ऐप्लिकेशन जमा करनी होगी।

- जिसके नाम पर प्रॉपर्टी का ट्रांसफर किया जाना है, सोसायटी में उसकी सदस्यता के लिए एक फॉर्म में ऐप्लिकेशन देनी होगी।

- प्रॉपर्टी ट्रांसफर करने के पीछे क्या ठोस कारण हैं, बताना होगा।

- ट्रांसफर से पहले सोसायटी के प्रति अपनी जिम्मेदारियां पूरी करनी होंगी।

- ट्रांसफर फीस अदा करनी होगी।

- जिस व्यक्ति को मेंबरशिप ट्रांसफर की जानी है, उसकी फीस भी देनी होगी।

- जनरल बॉडी मीटिंग में तय रेट पर प्रीमियम की राशि अदा करनी होगी (यदि ट्रांसफर परिवार के किसी सदस्य, नॉमिनी या फिर उसके लीगल रिप्रजेंटेटिव के नाम किया जा रहा है, तो उस स्थिति में यह शर्त लागू नहीं होती)।

- यदि आवश्यकता हो, तो 'नो ऑब्जेक्शन सर्टिफिकेट' (एनओसी) जमा करना होगा।

मैनेजिंग कमिटी या जनरल बॉडी सदस्यता का आवेदन या शेयर और कैपिटल या सोसायटी की प्रॉपर्टी में इंटरेस्ट ट्रांसफर का प्रस्ताव एक ही सूरत में इनकार कर सकती है

-यदि कानून के प्रावधानों या सोसायटी के नियमों का पूरी तरह पालन नहीं किया गया हो या फिर इस संबंध में सरकारी निर्देशों की अवहेलना हो रही हो।

- यदि सदस्य को अपनी ऐप्लिकेशन पर तीन महीने तक कमिटी या जनरल बॉडी की तरफ से कोई प्रतिक्रिया नहीं मिलती, तो उस हालत में ऐप्लिकेशन को स्वीकृत मान लिया जाएगा।

- यदि कानून या सोसायटी के नियम-शर्तों की अवहेलना करके कोई ट्रांसफर किया जाता है, तो उसे रद्द करार दिया जाएगा।

All about Reverse Mortgage

All about reverse mortgage - Rediff.com Business

In 2007, the finance minister of India introduced a concept well-known and widely accepted in the West: Reverse Mortgage.

Reverse Mortgage: What is it?

A reverse mortgage (or lifetime mortgage) is a loan available to senior citizens. Reverse mortgage, as its name suggests, is exactly opposite of a typical mortgage, such as a home loan.

How does it work?

In a typical mortgage, you borrow money in lump sum right at the beginning and then pay it back over a period of time using Equated Monthly Instalments (EMIs).

In reverse mortgage, you pledge a property you already own (with no existing loan outstanding against it). The bank, in turn, gives you a series of cash-flows for a fixed tenure. These can be thought of as reverse EMIs.

The specific format National Housing Board (the facilitator for housing finance in India) is promoting is one in which, the tenure is 15 years and the owner of the house and his/her spouse continue to live in the house till their death -- which can occur later than the tenure of the reverse mortgage.

Simply put, any senior citizen, opting for reverse mortgage will get annuity (the reverse EMI) from the bank for 15 years. After that, the annuity payments stop. However, they can continue to live in the house.

What are the features of this loan?

The draft guidelines of reverse mortgage in India prepared by the Reserve Bank of India [ Get Quote ] have the following features:

Any house owner over 60 years of age is eligible for a reverse mortgage.

The maximum loan is up to 60 per cent of the value of the residential property.

The maximum period of property mortgage is 15 years with a bank or HFC (housing finance company).

The borrower can opt for a monthly, quarterly, annual or lump sum payments at any point, as per his discretion.

The revaluation of the property has to be undertaken by the bank or HFC once every 5 years.

The amount received through reverse mortgage is considered as loan and not income; hence the same will not attract any tax liability.

Reverse mortgage rates can be fixed or floating and hence will vary according to market conditions depending on the interest rate regime chosen by the borrower.

How is the loan paid?

With a reverse home mortgage, no payments are made during the life of the borrower(s). Since no payments are made during the term of the reverse home mortgage loan, the loan balance rises over time.

In most areas where appreciation is good, the value of the home grows at a much faster rate than the loan balance. Therefore, the remaining equity continues to grow.

When the last borrower passes, or it is decided to sell the home and move, the loan becomes due. The ownership of the home is then passed to the estate or directed by a living will or will to the beneficiaries.

The beneficiaries now own the home and have to sell the home or pay off the loan. If the home is sold, the reverse home mortgage lender is paid off and the beneficiaries keep the remaining equity of the home.

What happens after the death of one or both of the spouses?

If one of the spouses dies, the other can still continue living in the house. If both die, the bank will give their heirs two options -- settle the overall outstanding loan and retain the house, or the bank will sell the house, use the proceeds to settle the outstanding loan and give the rest to the heirs.

How much of an annuity income can my house generate using reverse mortgage?

The banks have so far not indicated the interest rates. However, we can safely assume that it will not exceed the interest rates used for loan against property -- which is currently in the region of 12 per cent to 14 per cent.

What is a loan to value ratio?

Loan to value ratio means the percentage of loan that you will get for the value of the property that you pledge. The typical rate loan to value ratio is 60 per cent.

So, for e.g., if you pledge a property worth Rs 60 lakh (Rs 6 million), then the loan amount that you can get is Rs 36 lakh (Rs 3.6 million).

Does a person's age affect the amount of annuity paid?

It certainly does. Higher the age, higher the annuity! Everything else remains the same.

Why is this scheme not popular?

Recent reports seem to indicate that a very small percentage of senior citizens only seem to have taken advantage of the facility since its inception. This could be perhaps because better awareness had not been created about the product.

Secondly, the Indian banking industry caps the available loan amount at Rs 50 lakh (Rs 5 million), instead of providing for an equitable percentage of the property's value, and limits the loan period to a tenure of 15 years.

The product is still evolving and may take on new dimensions depending on how the banks wish to present its consumer appeal.

Saturday, February 5, 2011

Delhi doubles circle rates of properties - The Times of India

Delhi doubles circle rates of properties - The Times of India: "NEW DELHI: The Delhi cabinet Tuesday doubled the circle rates of properties -- the minimum selling price of a plot -- in the capital, a move that will help the government earn more revenue.

A meeting, chaired by chief minister Sheila Dikshit, decided to retain the earlier marked categories on which the circle rates were levied.

'We have decided to double the circle rates depending on the categories of colonies,' Dikshit told reporters after the meeting.

The previous circle rates based on the Municipal Corporation of Delhi (MCD) categorisation were Rs.43,000 per sq metre for Category A, Rs.34,100 for Category B, Rs.27,300 for Category C, Rs.21,800 for Category D, Rs.18,400 for Category E, Rs.16,100 for Category F, Rs.13,700 for Category G and Rs.6,900 for Category H."

A meeting, chaired by chief minister Sheila Dikshit, decided to retain the earlier marked categories on which the circle rates were levied.

'We have decided to double the circle rates depending on the categories of colonies,' Dikshit told reporters after the meeting.

The previous circle rates based on the Municipal Corporation of Delhi (MCD) categorisation were Rs.43,000 per sq metre for Category A, Rs.34,100 for Category B, Rs.27,300 for Category C, Rs.21,800 for Category D, Rs.18,400 for Category E, Rs.16,100 for Category F, Rs.13,700 for Category G and Rs.6,900 for Category H."

Thursday, January 27, 2011

Wanna see the pictures in big size? Just click on them.

Respected Viewer,

If you want to see any of these posts in big size----just click on that.

Welcome!

If you want to see any of these posts in big size----just click on that.

Welcome!

Tuesday, January 25, 2011

Saturday, January 22, 2011

Injustice---Indian Rent Control Acts

This legal injustice has killed many people,made many seriously ill ,deprived many people of their properties,who are real owner of these properties.

Let us take look into an article published by Sheikh Pervez Hameed ... 27/07/05--------------- Amendments to Delhi Rent Control Act (1958) in 1997 (a piece of legislation violating the fundamental right of an individual to property rights) has once again been put back. Strong traders lobby (main beneficiaries of status quo) has successfully capitulated the Urban Development Ministry. The Ministry has decided to hold back the move of tabling it in the monsoon session of the Parliament. The bill has been pending in Rajya Sabha for 8 years. Many owners are stuck with non-paying tenants due to this Act. Sad and heart rending stories of how tenants moved in on nominal rents and have become the owners of the properties abound. This bill had been passed earlier by both sessions of Parliament and the President had given his assent. Due to pressure from powerful tenant lobbies of Connaught Place, Chandini Chowk and South Extension, the bill was notified ... a formality for the passed bill to become law. Common Cause, a NGO sought direction from the Delhi High Court to the Govt. for notification of the bill. A committee of Rajya Sabha, on the issue "Can the Executive delay the enforcement of enactment passed by Parliament and assented to by the President" considered it as setting a unhealthy precedent by the Govt. by deferring the enforcement. Tenants of these areas pay Rs. 5 to 10 per month rental where as the prevalent rent in these districts are as high as Rs. 450/- per Sq. Ft. In most of the cases, tenants are now taking advantage of the bullishness in the reality market to illegally lease out the properties of which they hold lease. The genuine owner is not being given his due. The method employed is ingenious - using the franchise route. Delhi Rent Control Act in its current form is the single reason why Delhi landlords prefer to give their places on rent to foreigners. Foreigners go back, Indians stay on and use the Act to exploit the owners. This is for properties where rents are lower than Rs. 3,500/- per month. Over Rs. 3,500/- the law is balanced but the sentiment of good owner-tenant relationship has been systematically destroyed over the past few decades by the use of this Act. Generous donations to the political parties election funds by the tenant trader's lobby ensures that Government continues to deny its citizens the basic right to own and dispose of properties. Issues like this are of concern to the big time real estate investors as there is a lack of clarity. Govt. speaks differently, acts differently. Mind you, these traders are not so big in numbers, just well connected and very voluble.

Here is the link,U can directly go there also.

http://www.swagatamindia.com/real_est...

Here is the link of this foolish act--Delhi Rent Control Act-1958

http://bareacts.legalcare.in/index-27...

Here is the link of the amended act of 1995,which could not be implemented

http://www.vakilno1.com/bareacts/delh...

6 महत्वपूर्ण प्रोपर्टी टिप्स

6 महत्वपूर्ण प्रोपर्टी टिप्स

- कोई भी प्रोपर्टी किराये पर लें या खरीदें , उसका बिजली का मीटर चैक करवा लें, ताकि मीटर के साथ यदि कोई छेड़छाड़ की गयी हो तो उसका पता लग सके और पकड़े जाने पर हर्ज़ाना, जो कि लाखों रूपए में हो सकता है, वो आपको न भुगतना पड़े. यह चेकिंग BSES से ही नाम मात्र खर्चे से करवा सकते हैं. अपने बिजली के मीटर को चैक करते रहें, कहीं किसी पड़ोसी ने जाने अनजाने आपके मीटर में अपनी तार न लगा रखी हो.

- किरायेदार की पुलिस जाँच ज़रूर करवाएं. यदि किराया 3500/- रु. मासिक से कम है तो दिल्ली रेंट एक्ट में आने की वजह से मकान/ दुकान खाली करवाना बहुत मुश्किल होता है.

- रेंट एग्रीमेंट यदि 11 महीने से ऊपर का है तो उसे रजिस्टर करवाना ज़रूरी है. ध्यान रखें, यदि किरायेदार से रेंट एग्रीमेंट नहीं किया तो उस से मार्किट रेट का रेंट वसूल करना आप के लिए लगभग असंभव होगा .

- प्रोपर्टी खरीदते समय कागज़ात ठीक हैं या नहीं, इस की जांच Authorities/ Registrar Office से ज़रूर करवाएं. नोट नकली छापे जा सकते हैं तो कागजात क्यों नहीं?

- ध्यान रखें,आपके मकान /दूकान की ग्रिल, ख़ास कर मकान /दूकान के पीछे की तरफ से और ए. सी. के पीछे , घनी हो. चोरियां अक्सर ग्रिल तोड़ कर होती हैं .

- ध्यान रखें, मकान/ दूकान के निर्माण कार्य में आपके अंदाज़े से समय और धन, दोनों ज्यादा खर्च होंगें .

Either they can be friends---Or sales-persons.

Either they can be friends or sales-persons

Generally people go for being sales-persons

And there is nothing wrong in being sales-persons

But every thing is wrong in being crooked persons

Hiding things from others or telling half truths

Or distorting the truths

Or adjusting the facts according to their own need and greed

That is why I say that “Sales-persons” are generally “Foes” disguised as “Friends”

Irony is that generally we all are sales-persons

Irony is that we detest the people who sell their bodies for sex to earn money

Irony is that we never see that generally we all are selling our integrity, our honesty, our conscience just to earn money

And that is far far far worse than selling bodies for sex.

Friday, January 21, 2011

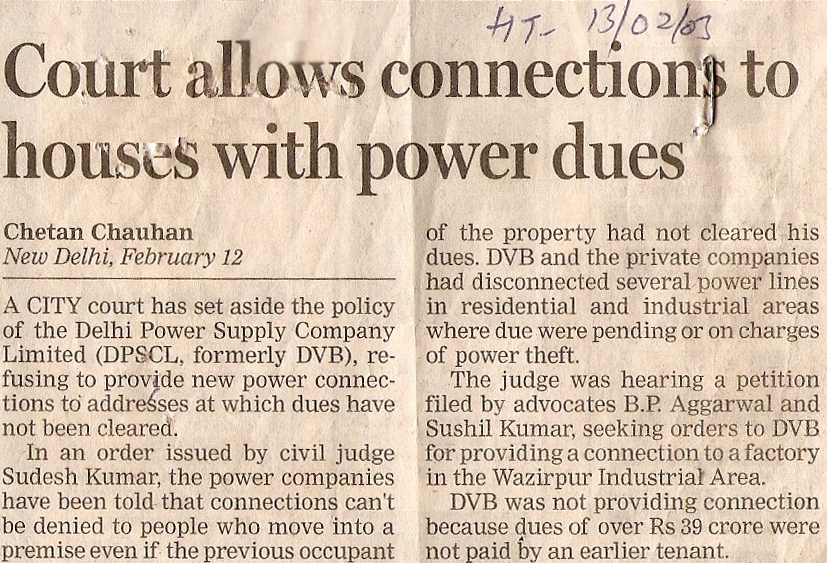

7 ‘enemy properties’ sold for just Rs 5 lakh - Hindustan Times

7 ‘enemy properties’ sold for just Rs 5 lakh - Hindustan Times

New Delhi, January 19, 2011

It does not take much to own a property in a prime location in the city. Here’s how: first you find a property that belongs to a person who migrated to Pakistan during Partition and bribe some MCD officers to get the property mutated. In no time, and for a mere R5 lakh, you can be the proud owner

of a multi-crore property in Chandni Chowk.

Thanks to some corrupt officials in the MCD, seven ‘enemy properties’ (those left by families who migrated to Pakistan in 1947) whose sale and purchase is not allowed (as government is the sole custodian of these properties) were allegedly purchased illegally by two persons. The MCD’s property tax department carried out mutation of the property, too. A copy of the mutation papers are with HT.

All the seven properties—number 177, 183 to 188 on Church Mission Road, Fatehpuri have been purchased by two persons at a cost of just R5 lakh.

Each property is about 3,000 sq feet in area. As per the orders of the Lt. Governor and Delhi government, any sale or transaction of ‘listed’ Enemy property is void.

A complaint in this regard has been filed by Deepak Mehta, a tenant of one property which were illegally purchased by two men who are residents of Greater Kailash II and Yamuna Vihar.

“These properties have been declared ‘Enemy Property’ and are listed as such on the Delhi government’s Revenue department’s website. But they have been illegally purchased by two persons. I’ve been complaining about it but the MCD has not done anything till date. Also, the purchasers, in connivance with MCD officials, illegally got the property mutated in the name of the illegal purchaser in 2009 after offering bribe,” said Deepak Mehta, the complainant and occupier of property number 185, Church Mission Road.

MCD’s City zone office and the vigilance department confirmed receiving a complaint in this regard. “MCD undertakes property mutation on the basis of duly registered property sale deed(s). As the part of the mutation process, the chain of ownership is examined. If there’s a clear chain of title of ownership only then mutation is done. In this particular case also, MCD examined the documents pertaining to sale of property as per aforementioned procedure. We have received a complaint and will examine the mutation done by us,” said Deep Mathur, director, press and information, MCD.

Mehta said the deputy commissioner (central), Delhi through SDM (Daryaganj) Delhi had written a letter to the deputy assessor and collector of MCD’s house tax department in 1998 that all seven properties are ‘Enemy’ properties and thus immune from sale, seizure. “However, the officials of the house tax department removed the letter of the SDM from the file and illegally mutated the property. Strict action should be initiated against them,” said Mehta. A copy of this letter is also with HT.

Pay Fine for tinkering with building plan and get Regularization - Hindustan Times

Fine for tinkering with building plan - Hindustan Times

Hindustan Times

New Delhi, January 21, 2011

This one is for those who built their houses on whims and fancies. If you installed a washbasin where it was not supposed to be or constructed a whole new wall just to get another room, the MCD will hunt you down soon and slap a fine. Finalising its budget estimates for 2011-12 at a special

meeting of the MCD's standing committee, the civic agency has decided to survey all properties in the city including posh approved colonies to find out if any unauthorised construction has been carried out.

Property owners who, after getting their building plan sanctioned, made certain deviations to the original plan by constructing an additional partition wall, a new wash basin, extended their balconies, etc., will be fined. The civic agency is hoping to earn R25 crore through this exercise.

"There are thousands of property owners who had got their building plans sanctioned many years back and have made many changes to their houses. Rather than demolishing those structures, we want them to get it regularised by paying a fine. A survey to ascertain the deviations made in those properties will be carried out this year," said Yogender Chandolia, chairman of MCD’s Standing Committee.

Officials said the fine can range between R5,000 to R1 lakh, depending on the deviations.

"There are a number of property owners whose plans were cleared when the Master Plan of Delhi (MPD) 2001 was in place. But they carried out construction, which were not permissible under the MDP 2001 but are covered under the MPD 2021. These owners will now have to shell out lakhs of rupees to get their buildings regularised, otherwise the construction will be termed illegal and demolition action can be carried out there," said a senior MCD official.

Property owners in a number of posh colonies such as Greater Kailash I, II, Lajpat Nagar, East of Kailash, Jangpura, New Friends Colony, Saket, Malviya Nagar among others have constructed third floors. This is covered under the MPD 2021 but was not part of the building plans when sanctioned.

"They will have to pay a fine for getting the third floor regularised too," added the official.

Fire Safety Measures for Home

‘Precaution is better than cure’ this saying holds a lot of importance in everybody’s life. People should be aware as well as equipped with necessary measures to safeguard themselves and the people around from accidents. Fire accidents are the most common ones that cause huge damage to life and property. These can be curbed to a great extent following certain simple measures. We in this write up offer you measures to prevent fire accidents that can take place at your home.

Causes:

Before taking any safety measure against fire, it is important to identify its possible causes. The following are the few reasons that may become a cause of fire at your home:

Absence of fire alarm

Alcohol is a possible cause of fire. About 40% of fire accidents at home are caused by alcohol.

Delayed actions: Most of the fire victims die because of inhaling toxic smoke and poisonous gases for a long time rather than dying of burns

Most of the fire accidents take place in the kitchen owing to wrong handling of gas cylinders, non-switched off stoves etc

Smoking is one of the major causes of fire accidents

Short-circuiting

Preventive Measures:

The following are the safety measures that you must observe at your home, which will protect you and your family from the threats of fire accidents:

√ Install fire alarms at all the proper places at your home such as near bed rooms, kitchen and fire places.

√ Install proper system of fire extinguisher and make sure that each member of the home knows how to operate it.

√ Keep the hazardous objects such as match sticks, lighters, stoves and flammable chemicals out of the reach of children.

√ Keep the non-cooking objects such as towels, plastic utensils away from the gas stove.

√ Make sure that the cigarette butts are completely extinguished before disposing them.

√ Avoid fireworks inside the premises.

√ Make provision for emergency exit in the home.

√ Provide proper training to children regarding how to safeguard themselves in case of a fire breakout.

√ Turn off the gas stove before leaving the home and before going to sleep each night.

√ The electrical appliances shall be properly operated.

√ Gas cylinders should be kept in safe places and should be operated with care.

√ The wiring of the house should be checked on regular basis in order to avoid short circuiting.

What to do in case of a fire breakout?

In case fire takes places in your home, observe the following rules to reduce the damages caused due to it:

Close down all the doors and windows of the home once everybody is out of the house. This will stop the oxygen supply and thus stop the fire from spreading further.

In case your clothes catch fire, lie down on the floor and start rolling to put the fire to an end.

Switch-off the electrical appliances in case of fire.

Thus, by following a few simple measures you can avoid fire related accidents and thus safeguard your family and your home from any kind of fire threats.

4 Diplomatic House Buying Tips

The tumultuous path of buying a house is nothing short of a nightmare. All the hurdles and vagaries in the trail of buying a house can leave a buyer feel burdened & strenuous. So, it is quite essential to plan wisely for buying home in order to be relieved of all the obstructions coming in the path.

Some Handy Tips To Make Road To Your Dream Home Easier:

► Tip 1

► Tip 1

Never let the seller know that you are very much interested in buying the property. If you show too much interest in the property, the buyer will get an idea that you are ready to pay any amount to buy the property. So, you are expected to play the game well. You need to be tactful and a diplomat. Where on one hand, you are not expected to show too much interest, on the other hand, you are also expected to not let go the property. Act as if you have many options and the property is not only the one.

► Tip 2

If you wish, you can quote a low offer, but never expect the seller to agree on that particular offer. As per the market value & requirement, the seller will finalize the deal. Changes in price are possible, if you negotiate well. You need to be really careful while transacting. Even if your real estate agent tells you that the price being quoted is low, then also he has to take that offer to the vendor as per law.

► Tip 3

This is a godfather rule that the person standing next to you shouldn’t have an idea about what’s going in your mind? Don’t even let your agent or seller know that what is the highest price that you are willing to pay for a particular piece of property? Keep everything to yourself. Don’t fall in trap. This factor makes a major difference in house buying.

► Tip 4

Don’t neglect other offers. Keep track of all other properties available. It is possible that you get to strike a better deal for a better property.

Hence, these are the main points that must be kept in mind while starting the search of a house. Apart from this, avoid making hasty decisions in the matters of property.

15 Great Tips For Buying Property

"15 Great Tips For Buying Property "

1) Research is the key

Always do research. You can never do enough research. A lot of people dive into the property market head first and blind folded, and that’s when people make bad purchases. If you like a property, find out about the surrounding area; find out the local crime rate, find out how much properties in the area recently sold for. Find out EVERYTHING. There are tonnes of websites out there that will give you all these details at no cost.

2) Prepare yourself financially

Financially prepare yourself before you make any offers- get financially sorted. Make sure you can afford the property. Make sure you have taken every cost into consideration, like conveyancing solicitors, stamp duty, survery fees, Estate Agent fees etc. Most importantly, make sure you can get the financial backing you need.

3) Structural Survey

Always get a structural survey done. With the newer homes, the basic or mid-ranged survey is fine. But with older properties, definitely get the higher-level inspection. Sure this may add expenses onto your limited budget, but it could potentially save you thousands. Regardless, most Mortgage lenders will insist on a structural survey, as they won’t want to help you finance a house that’s about to fall apart.

4) Property fittings

Make sure you ask what comes with the property before you make an offer. A lot of houses are presented beautifully, especially with fitted bathrooms and kitchens. You may get a nasty shock when you move in only to find the previous owners took the fittings with them.

5) Stay away from the asking price

Never offer the asking price, even if you’re in love with a particular property. Sellers/Estate Agents usually add on a few lakhs from the actual value of the property, because they expect offers to always be below asking price. Be risky, and make a cheeky offer- you maybe surprised.

6) The Property Market

Find out how long a property has been on the market for from your Estate Agent. If a property you’re in love with has been on the market for a long period of time, ask yourself why; be suspicious. If the property is legit, and for some odd reason it’s not selling, then make a low offer.

7) Control your emotions

Never act overly keen to either the seller or your Estate Agent. The Estate Agent and seller both have one thing in common- they want the buyer to spend as much as possible. Remember, the Estate Agent is working for the seller, not the buyer. If you act overly keen, they will make you spend more money than necessary. Buying property is like playing a game of poker- you need to play the game with a face of stone.

8.) Be patient

Don’t let your patience get the better of you. Never rush into buying a property; buying a house is a big deal and will effect your life. There is an art to buying property, and patience is a big part of it. Impatience leads to expensive and inadequate purchases. If your patience is the direct reason of losing out on a deal, don’t worry, properties come and go on the market. On the other hand, your impatience could be the direct reason of making a bad purchase, and consequently throwing your money down the drain.

9) The future is important

Think about the unforeseeable future. The property market is a very uncertain area. Interest rates can increase at any time, and that will have direct impact on your monthly mortgage repayments. You may be out of work for a period of time, would you still be able to afford the monthly mortgage payments?

10) An empty property looks so much different

Imagine the property is empty- do not be fooled by props a seller has strategically planned. Once a house is stripped from all it’s wrapping, you maybe surprised how different she, I mean, IT, looks. Check behind and under the furniture, because you never know what surprises maybe hidden away- peeling wallpaper, stained carpets etc.

11) Don’t forget your neigbourhood

Are you looking for a peaceful area? Remember, an Estate Agent is working with the seller to get a maximum sale value- they will arrange viewings at optimum times. When you view a property, the surrounding area may be quiet and peaceful. Consider what the noise maybe like at times you haven’t been there.

12) Damp properties

Smell for dampness. Touch the walls; feel if they’re damp. Always be suspicious if a home is overly heated and sprayed with overpowering fragrances.

13) The roof can be costly to fix

Check the tiles on the roof. A lot of people neglect the roof when inspecting a house, and that’s exactly where a lot of people have to shell out a lot of expenses. This especially applies to older properties.

14) Location is just as important as the property

Finding the dream house is always great. But what about your dream location? Does it contain all your essentials, like a local groceries, schools etc. Don’t just focus on the property; focus on the bigger picture. Make sure the local area is equipped for your requirements.

15) Shop around for property

You can never find the right property after one viewing; even if you think otherwise. Make sure you take your time looking at several difference properties. Don’t just look in one area, be a little open minded and open yourself to possibilities. You’ll get a better idea of what your hard earned cash can actually get you.

Thursday, January 20, 2011

Ten Tips For First Time Home Buyers

Ten Tips For First Time Home Buyers

Are you like most Indians? If so, chances are that you have never bought a home before, i.e., you are a first time buyer. Buying a home is going to be the biggest investment that you will make in your life. No wonder this process is financially and emotionally draining. These tips will help you during your home buying experience.

1. Don’t budge from your budget

There is too much choice in the real estate market in India – you must understand what is your budget so that you can narrow your search into a manageable process. Otherwise, your real estate broker will spin you around. Give the broker your budget and tell them that its not movable. Don’t believe them when they say your budget is too low. There are properties of all types available in India today.

The budget is not just the cost of the property – it must include numerous non-obvious costs such as broker fees, lawyers fees, stamp duty, registration fees and home insurance premium. All these payments will come out of your pocket.

If you are buying a new home, you will also need furniture, fittings and gadgets for the home. Alternatively, if you are getting an old home, there might be renovation or redecoration costs involved. In either case, these are upfront costs that many people ignore during the home buying process but should be factored in.

2. Affordability – “I have a great home, but no money to eat”

There is no point in searching for the house of your dreams if you cannot afford to live there - you must also think about whether you have enough cash flow to support your lifestyle, after you have paid for the property.

Do not stretch yourself and take a personal loan to fund the down payment towards the property. This will only increase your risk exposure. Rather, you should ensure that you can naturally afford the down payment through your savings.

Additionally, don’t stretch your budget to get a more expensive home because that will mean stretching your EMI payments. Remember to keep your EMI manageable so that you can continue to afford the lifestyle that you are accustomed to and to pay other bills that you will incur.

3. Location, Location and Location – the three most important rules of real estate

Location is key. It will affect the quality of life that you have in and around your home. Additionally, a better located property will get a much better resale value if you decide to sell.

Before you put in your life’s saving into buying a property, you might want to consider renting in your desired location for a few months. It will give you a good flavour of what life could be like in the area.

When thinking of location you must consider the following: proximity of schools, your commuting time to and from work, modes of transport around the property, local amenities and shopping convenience, proximity to family, friends and your community, noise levels around the area and avoiding undesirable irritants (such as the proximity of garbage dumps, electrical sub-stations, sewage canals).

Finally, if you are viewing the property on a weekend, the traffic and noise situation might often be very different from the weekdays, so do check the desirability of the location at different days and times of day.

4. Define your specifications – “I want a mansion, overlooking the hills, with mango orchard around me”

Prioritize what is important to you. If you are married, collectively agree with your spouse on what you are willing to compromise on. Otherwise, smooth talking real estate salesmen will take advantage of you by showing you too many different properties on criteria that will not be important to you.

Is a large kitchen important to you? Do you need an attached bathroom to every room? Do you want lots of storage capacity? Do you need a study for your home office? Do you need a terrace or garden for the kids to play in? Do you want to buy an old home which might have old construction and aged plumbing, or you will only look at new homes which will be modern but you will pay a premium for the freshness?

5. Be patient – resist the urge to get angry and break things around you

The home buying process can be time consuming and complicated. If something can go wrong, it will. But, if you are mentally prepared for it, then you will not be surprised when delays happen. Budget at least 3 to 6 months for the process, especially keeping in mind the timing of when you absolutely need to move into the new home.

Do not get frustrated if you do not feel fully in control of the process. Remember, that you are going to be at the mercy of the real estate brokers, the developer, the home loan lenders, lawyers and other intermediaries. Money, documents, contracts and agreements need to move around all these different players in the process. Things will not always move at your pace, but at the pace that these intermediaries choose.

Just remember to keep smiling through the process - think about how much you are going to enjoy living in your own house when you finally can call it home.

6. Viewings – if you like it, see it twice!

Of course you are not going to buy a property without seeing it. But, don’t make the mistake of taking your entire family with you the first time around. If they get over excited, the real estate broker is going to sense this, and then will exploit this to his/her advantage.

You must also visit the property at least a few times. After all, this is a big decision for you. You are going to be spending the next few years of your life here. Go to the property 2-3 times, at different times of day. Note how you instinctively feel about the property. Why do you feel this way? Can you really call this place home? Maybe at your second or third visit you can take the extended family with you to get their reactions as well.

Maintain a viewing checklist on which you can rank the different properties you are visiting on the criteria that you have prioritized. Remember, you do not want to regret that you were forced into a decision to buy under pressure from a real estate broker or because you had very little time to view the property.

7. Jadoo – learn how square footage can magically disappear

Get familiar with the language and conventions used in real estate. When some one gives you an area for the property, always ask them what definition of area they are using. Here is why this is important.

Typically, the area that you pay for is higher than the area that you actually get. For instance, you will pay for a 2,000 square feet flat, but your usable area might only be 1,500 square feet. You will face a reduction in the area. In this example its 25%, but it could even be more in actual cases.

No need to worry, you have not been defrauded. The square footage that you have lost is your share of the communal facilities on the floor like walls, corridors, lifts etc.). But, you will have to pay for the entire area, including the area that is lost.

Always ask what is the carpet area that you will get, i.e., the area over which you can actually spread carpet across the entire floor if you so wanted to do it. This, effectively, is the area that you will have for your end use.

8. Show me the money - review your financing options simultaneously

Just finding the right home is of no use to you if the deal falls through because you have not organized your funding. Often you will need to demonstrate that you have access to the funds to finance your purchase. Therefore, organize your funds before you need them.

If you are self-funding your purchase, ensure that you have enough funds that you can access at short notice if your deal comes through and you are required to pay immediately.

If you will need a home loan, file an application with your chosen lender and get approved for the loan. You can get approved even if you have not yet identified the property. This will save you time and emotional hassles later on in the process. Typically, such approvals last for 6 months which should give you sufficient time to identify a property.

9. Black, white and grey areas - buying directly from the developer vs. the investor

These are boom times for real estate development in India. Developers are coming up with new projects all the time. Many investors have bought many properties for investing purposes. You need to understand that there is a difference in buying directly from the builder versus from the investor in a property.

If you buy property directly from a developer in a project that is under construction or nearing completion, its likely that you will not have to pay any cash component, and the entire payment can be in cheque.

On the other hand, if you buy from an existing owner of the property (even if its under-construction), the owner will expect to earn a return on his/her investment, and might expect a large part of the payment in cash. You need to be aware whether you are capable of making cash payments. This is a reality in India and in many cases you will not be able to avoid it.

10. You are going to live long – your current purchase doesn’t mean “game over”

As your you and your family grow, so will your needs. You might get married, have kids, your parents might move in with you. Some unplanned events might also occur; for instance, you might get transferred to a new city.

Don’t see your current purchase as a dead end. You can upgrade to a different property in a few years. Maximise what you need to fulfill over the next few years. Nobody has seen the future - you will not be able to ascertain whether this property will suitable for your 10 years from now. Remember, you can always sell this property and use the sale proceeds to get another property.

You might feel nervous about your first home purchase. With a little bit of attention to detail and awareness, you can become more confident even before you start the process. And of course when the deal finally closes, savour the positive emotions. There is absolutely no substitute for the joy and pride that you will experience at your first home purchase.

Subscribe to:

Posts (Atom)